Eye on electricity

Spring outlook: Understanding the change in wholesale price risk

- Generation

- Wholesale

While rain over the weekend was welcomed, national hydro storage is still low. As a result, this week, the Electricity Authority changed the risk assessment of wholesale electricity prices in our weekly snapshot from green (low risk) to amber (medium risk). Without significant rain and snowmelt to increase hydro storage, more thermal generation will be needed in the coming months, which will mean higher wholesale electricity prices. The security of supply risk for energy – having enough electricity to meet demand – remains at ‘green’.

This article explains what’s behind this important change in our view.

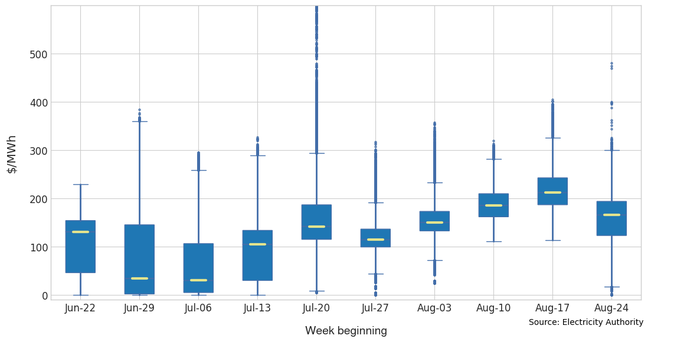

Summary: spot prices have increased over the last few weeks as hydro storage has fallen

There were very low inflows into the hydro lakes throughout August. To conserve water, more coal and gas generation was used, pushing up wholesale spot prices (Figure 1).

These prices are wholesale prices and do not impact what most people pay for electricity. Most purchasers of electricity on the wholesale market insulate themselves from these prices through hedge contracts.

Looking towards 2026, there is below average snow cover in the catchments that supply our largest hydro storage lakes and La Niña conditions tend to lead to low rainfall in the South Island.

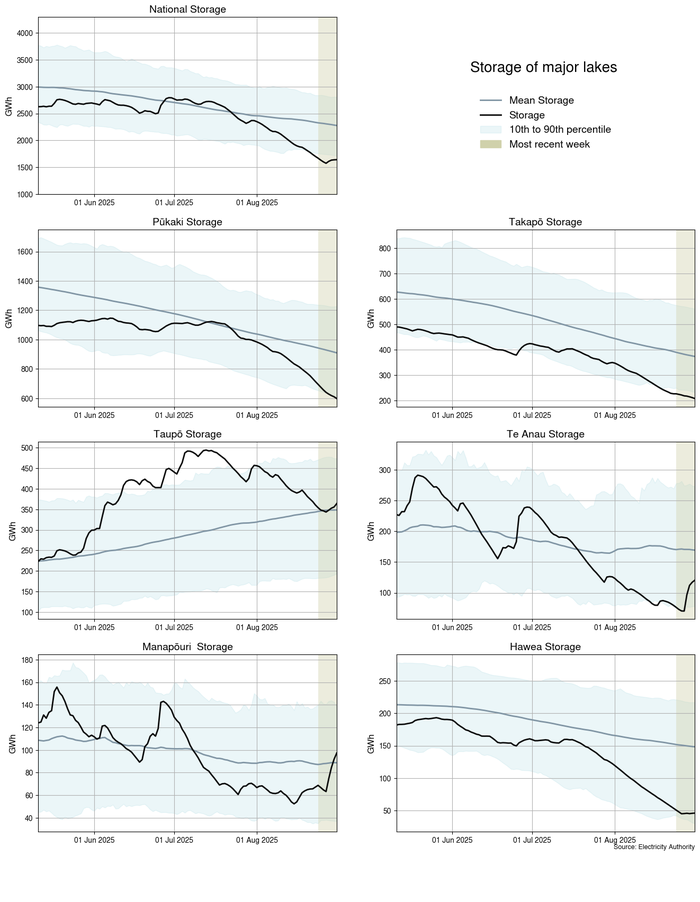

Most hydro lakes are well below mean levels for this time of year

Hydro generation usually generates more than half of New Zealand’s electricity. Our largest hydro schemes are hugely valuable to ensuring electricity security of supply because, unlike wind and solar generation, they’re able to store the energy (as water) for later use. This storage naturally fluctuates throughout the year, with storage generally drawing down over autumn and winter as our electricity use increases, and refilling again in spring and summer as the snow melt lifts lake levels and electricity demand lowers. Most of the hydro storage lakes are located in the lower half of the South Island, in the Otago, Canterbury and Southland alpine regions. Lake Taupō is main hydro lake in the North Island.

Currently all the hydro storage lakes, except Lake Taupō, are below mean storage for this time of year. Figure 2 shows hydro storage at each lake on 31 August 2025. All catchments have been declining steeply since mid-July. Currently, each lake is:

- Takapō 27% full

- Pūkaki 34% full

- Hāwea 16% full

- Te Anau 45% full

- Manapōuri 62% full

- Taupō 63% full.

Only Lake Taupō has been above average over June, July and August. Levels of lakes Hāwea, Takapō and Pūkaki have been mostly below their mean since January.

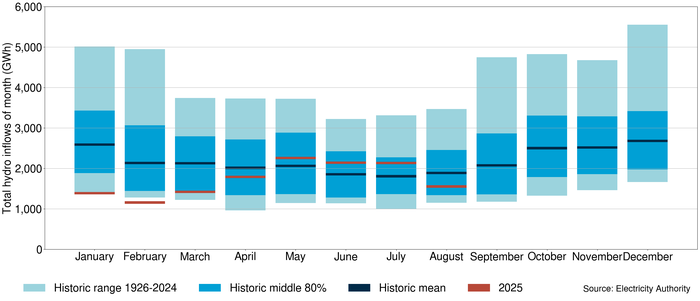

Inflows have been low in August

Hydro storage has declined following low hydro inflows in August 2025. Figure 3 shows how this year’s monthly national inflows compare to the historic range.

Inflows were well below the historic mean from January through to March. This improved throughout the April-July period, with inflows mostly above mean. However, inflows have reverted to low again for August.

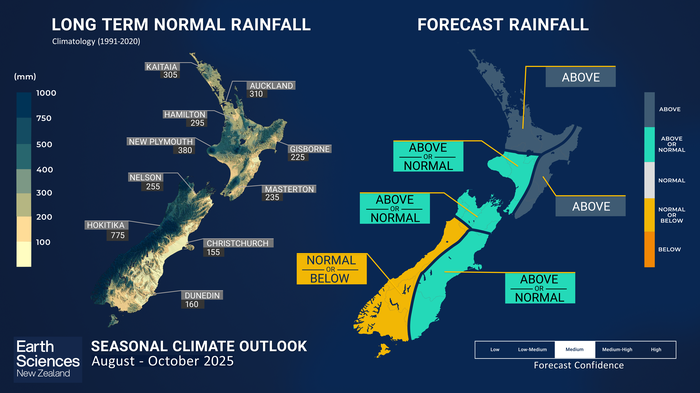

Rain is expected, but overall the outlook is dry for hydro lake regions

Recent rainfall is expected to continue into early September, with NIWA predicting above average rainfall for the west of the South Island until roughly mid-September. However, the three-month outlook is for drier than normal conditions for this area (Figure 4).

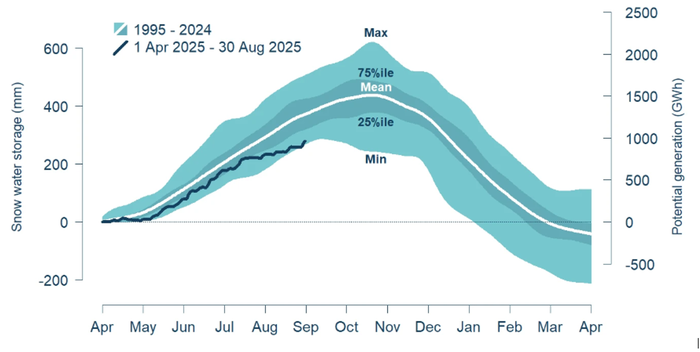

Currently the Waitaki snowpack is lower than average

Snowmelt helps refill water in the Waitaki and Clutha catchments, and to some extent the Manapōuri storage lakes. Meridian Energy estimates the generation potential of the current snowpack at the Waitaki catchment (Figure 5) is below average at 968GWh, which is close to the lowest recorded snowpack for this time of year.

If the snowpack feeding the Waitaki catchment remains low, and rainfall is below average, this will reduce the water available for hydro generation in winter next year.

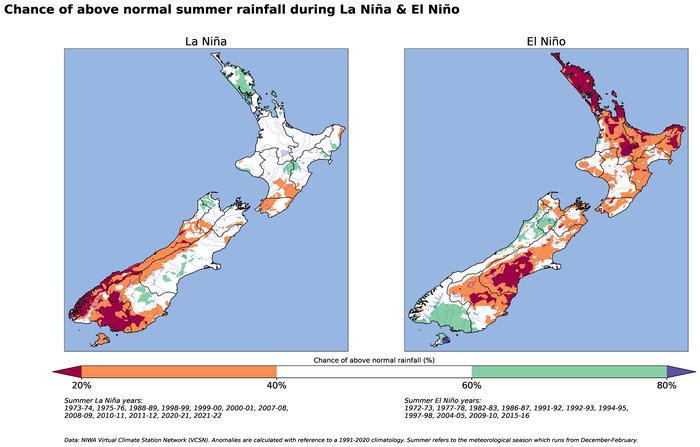

Longer-term forecasts show increasing odds for La Niña over summer

Large-scale atmospheric conditions can give an indication of whether rainfall will be higher or lower than normal. One of these is the El Niño Southern Oscillation (ENSO).

NIWA’s latest climate outlook says:

ENSO-neutral conditions are the most likely outcome (about a 60% chance) over the forecast period (August – October 2025), but compared to ENSO outlooks issued last month, chances for La Niña to emerge by the end of the calendar year have increased.

La Niña conditions over summer typically see below average inflows in the South Island hydro catchments (Figure 6).

The security of supply risk for winter 2026 will increase if the hydro lakes don’t sufficiently refill and if a La Niña summer occurs.

Forward prices and thermal generation have increased

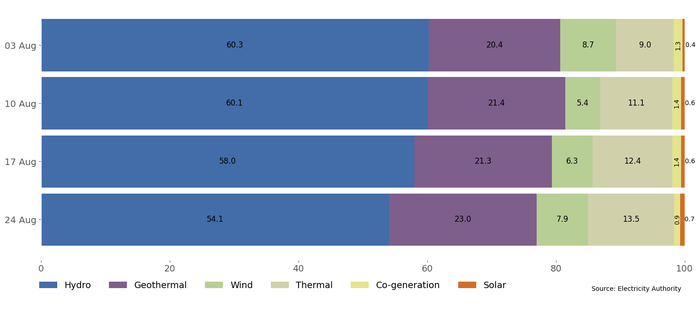

The electricity market is already responding to the increasing risk of insufficient rainfall and snowmelt. In recent weeks, thermal generation has increased, and hydro generation has decreased (Figure 7). This has helped preserve hydro storage.

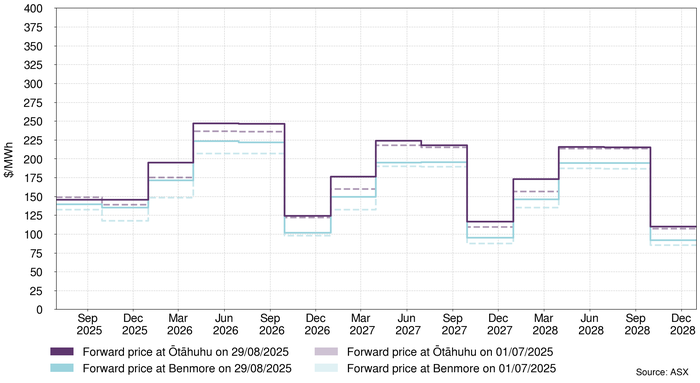

The forward electricity prices give an indication of likely future wholesale prices. Figure 8 below shows forward prices for the March and June 2026 quarters also increased by $19/MWh and $11/MWh (Ōtāhuhu) respectively over July and August. The 2026 winter quarters are significantly above winters in the next two years, suggesting elevated risk for winter 2026.

Ensuring there’s enough power in the system

The Electricity Authority focused on ensuring New Zealand has a reliable and continuous electricity supply. Going into this winter, we worked to help industry prepare and to ensure there was enough power in the system to meet the country’s electricity needs. We also have a host of initiatives underway to continually improve market settings to strengthen the security of supply.

While there’s no need to spring into action just yet, we’re monitoring the security of supply closely to make sure the electricity system is responding in a way to manage any further tightness in our electricity supply and will continue to provide updates.

Related News

Policy changes to strengthen dry year risk management

The Electricity Authority Te Mana Hiko has approved changes to the Security of Supply Forecasting and Information Policy to improve certainty and better suppor…

Electricity Authority launches new consultation on non-discrimination obligations

The Electricity Authority Te Mana Hiko has launched a further consultation on certain aspects of the proposed non-discrimination obligations, which are aimed a…

Are ASX futures prices too high?

In the New Zealand wholesale electricity market, participants can buy and sell hedges as a possible method of managing risk caused by spot price volatility.