Eye on electricity

Are ASX futures prices too high?

- Wholesale

- Prices

In the New Zealand wholesale electricity market, participants can buy and sell hedges as a possible method of managing risk caused by spot price volatility. Most hedge contracts involve two parties essentially agreeing to trade contracts for some volume of electricity at a fixed price for a set period of time in the future. For example, on a particular day in 2025, an industrial electricity consumer might buy a 5MW contract at $200/MWh for the period of Q3 of 2027.

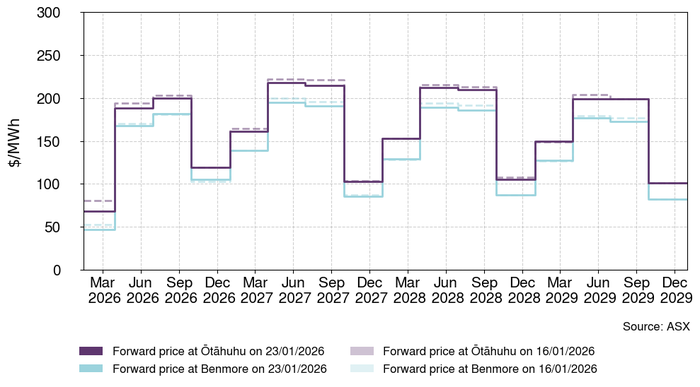

Market makers and participants regularly trade and offer hedges on the ASX futures market and this trading activity is used to price these products. The ASX draws on executed trades and bid-offer activity to produce closing prices for different types of hedges. These published prices form the basis of the forward price curve (Figure 1), which reflects the market’s collective expectation of future spot prices. The forward price curve is often used as a reference point for trading over-the-counter hedges. This price discovery is an important element in a competitive market because it ensures market prices are set by expected supply and demand dynamics.

Risk premia shaping ASX futures prices

Pricing hedges involves consideration of various risk premia associated with holding the contract position and exercising it over its duration. In this context, a risk premium is the premium from pricing a hedge contract for a higher return proportional to the risk a participant is taking on by agreeing to the contract. These risk premia involve consideration of hedge location, shape, hedge market liquidity, spot price volatility, possible scarcity and ASX market volatility.

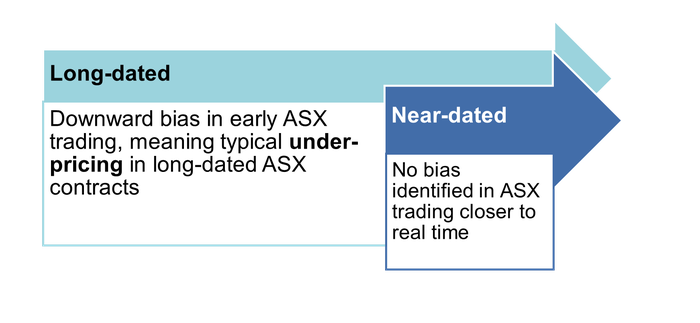

Near-dated futures tend to react strongly to current market conditions such as hydro storage levels. In contrast, long-dated futures incorporate expectations about how the market may evolve over time based on information such as new generation plans, gas availability, demand growth and potential changes in the supply mix.

A more thorough explanation on what contributes to futures prices can be found in this previous Eye on Electricity article.

Long-dated ASX futures have been underpriced historically

It is not possible to know with certainty how accurate currently-traded futures prices are because expectations on future spot prices are inherently subjective. In a competitive market, futures prices represent the collective view about current and future market conditions. There will always be periods when futures are over or under priced relative to eventual spot prices. The important consideration is whether these highs and lows tend to balance out to a neutral view over the long term.

In 2025, the Electricity Authority commissioned an Infometrics report to assess whether ASX futures have displayed any historical pricing bias. Their analysis indicated that long-dated ASX contracts have been generally under-priced (Figure 2). This means parties have generally been selling long-dated hedges for cheaper than the eventual spot price reality. A similar pattern has been observed in the over-the-counter hedge market, where parties that mostly sell hedges have incurred large losses in some years as a result of this under-pricing.

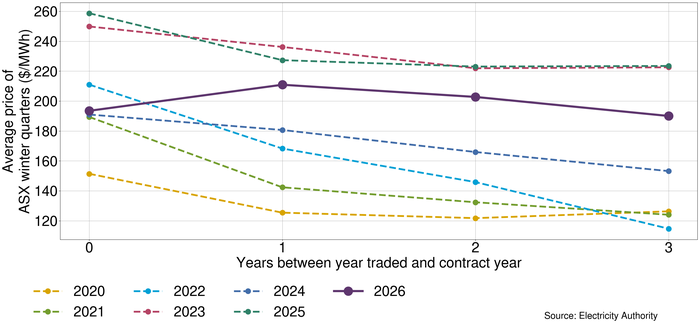

Currently-traded long-dated futures prices are higher than some historic long-dated prices

While ASX prices have historically tended to be under-priced, futures prices increased following the period of extreme prices in August 2024, as traders factored in a higher perceived risk of similar events occurring in the future. Current futures for the next winter (winter 2026, less than one year between year traded and contract year) are broadly similar to those of previous years, but longer-dated winter futures (1+ years between year traded and contract year) are trading at higher prices than in some previous years (Figure 3). However, given the historical pattern of under-pricing, these higher prices appear consistent with an unbiased, competitive market.

Futures prices are appropriate given market conditions

ASX futures prices have increased for longer-dated futures, but that does not necessarily mean prices are inappropriately high. When we consider whether futures prices are high, we must consider historic spot prices, new generation being built, projected demand growth, and the probable cost of different types of generation.

The generation investment pipeline shows that increasing electricity demand and existing generation retirement are expected be met by new wind and solar generation over the next few years. However, this increasing reliance on intermittent generation will likely increase volatility in spot prices. These more volatile spot prices are likely being factored into futures prices and increasing the risk premia.

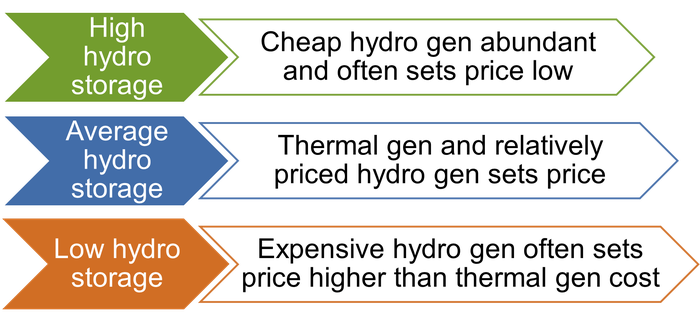

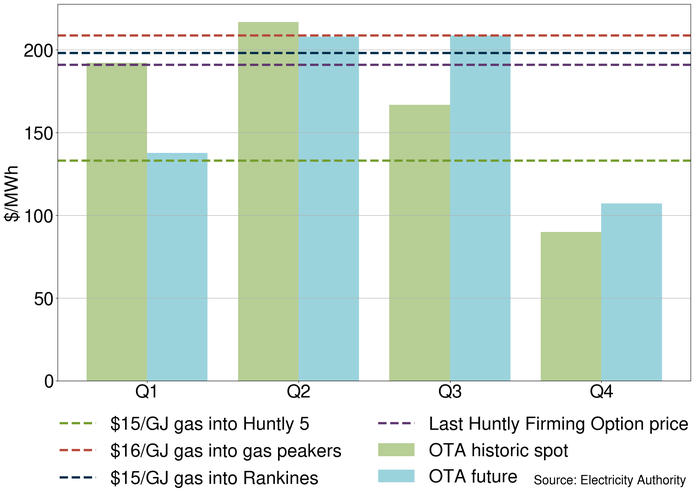

Even with more new renewable generation coming online, New Zealand will still need thermal generation in the immediate future to provide firming. This will especially be true during winter evenings when the sun has gone down or when wind is low and battery storage isn’t sufficient. Thus, gas and coal prices will continue to have an impact on the wholesale electricity spot prices. Typically, the wholesale spot price in winter quarters (Q2 and Q3) is set by thermal generation and hydro generation that is priced relative to thermal generation (Figure 4).

Figure 5 puts currently-traded futures prices in the context of current and probable future market conditions. Only Q3 futures seem especially high compared to what we would expect based on historic spot prices. Q2 and Q3 futures, which encompass the winter months, are priced similar to the estimated costs of running most thermal generation. Overall, when considering the current gas market and various deals the gentailers have made, Enerlytica estimated (subscription required) that Contact will pay about $16/GJ for gas in 2026 and Genesis paid about $15/GJ in 2025. At these gas prices, it would cost about $209/MWh to run the peakers and $198/MWh to run the Huntly Rankines on gas. In January, Enerlytica reported (subscription required) that the Huntly Firming Option long duration strike price was $191/MWh.

In August 2024, prices were extreme due to very low hydro storage and gas scarcity. There is always dry year risk around hydro storage levels, but gas scarcity risk has been building since the Pohokura gas outages in 2018. This has pushed up gas prices and increased the cost of gas-fueled thermal generation. It makes sense that Q3 futures prices have increased given that gas scarcity will continue to be an issue in the immediate future.

The introduction of the Huntly Firming Options, which guarantee access to coal-fueled generation, will improve security of supply. However, they can only decrease the electricity price as low as the cost of generating with coal. Therefore, there is no reason to expect the Huntly Firming Options to significantly decrease pricing; rather, they help limit the possibility of even higher spot prices in the event of severe gas scarcity.

Considering current and expected future market conditions, ASX futures prices do not appear to be inappropriately high.

ASX prices are being monitored

The Electricity Authority will continue to monitor ASX futures prices. We have started a monthly Hedge Market Summary which reports on both ASX and over-the-counter hedge market activity. The purpose of this reporting is to make the hedge market easier to understand and support participants in making informed trading decisions.

In addition, the Authority is undertaking a review of Market Making arrangements to improve price discovery and competition in the electricity futures market. Decisions on the review will be published in April.

Related News

Hedge disclosure certificates due by 30 June

Participants in the hedge market are required to submit an annual hedge disclosure certificate and must do so by 30 June 2026 under clause 13.230 of the El…

Upcoming consultation papers on battery energy storage systems and hybrids

The Electricity Authority Te Mana Hiko will soon be seeking feedback on a package of papers to support the role battery energy storage systems and hybrids play…

Space weather and the power system

Space weather has the potential to cause significant disruption to New Zealand’s electricity system. While rare, severe solar storms that reach Earth may affec…