Eye on electricity

How thermal generation costs affect wholesale electricity spot prices

- Generation

- Prices

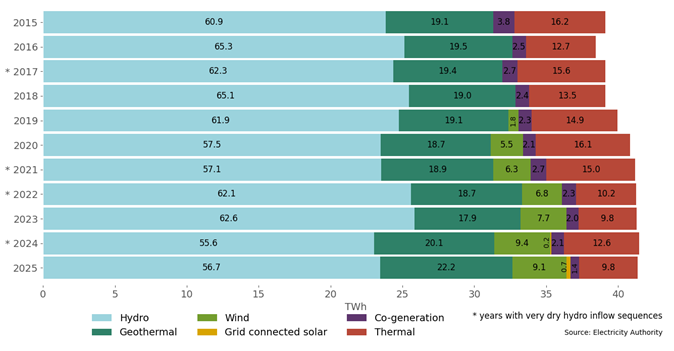

New Zealand’s electricity is generated from hydro, wind, solar, geothermal and thermal fuels. Thermal fuels include coal, natural gas and diesel and are an important part of ensuring the security of electricity supply. During winter months, thermal generation and hydro generation often set the wholesale spot price. This article explains the relationship between the cost of thermal generation and wholesale electricity spot prices.

Over the past few years, the amount of thermal generation used in New Zealand has decreased slightly as more renewable generation has been built (Figure 1). However, thermal generation still makes up at least 10% of the generation share and that rises during dry years. This is because thermal generation is a key part of firming renewable generation, which relies on weather patterns.

We estimate thermal generation costs using fuel prices

The cost of thermal fuel is one of the primary factors that determines how much thermal generation costs to run in the short-term. This is called the short run marginal cost (SRMC) of the generation. We publish our estimated SRMCs of different thermal generation every week in our Trading conduct reports. A detailed explanation of how we calculate SRMCs is available in Appendix C of the Trading conduct reports.

Overall, the Authority considers the monthly cost of the fuel, the efficiency of each generation unit and the estimated operation and maintenance costs of the generation units. Some units, like the combined cycle gas generators (Huntly 5 and the newly retired Taranaki Combined Cycle) are more efficient than others (the thermal peakers). More efficient units have cheaper generation costs for the same fuel prices. Coal prices are set in international markets, but New Zealand gas prices are set domestically.

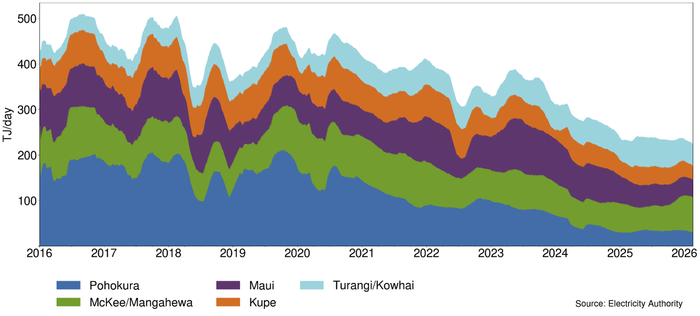

The 2018 Pohokura gas outages and the decline in New Zealand gas production

The Pohokura gas field was one of the major gas fields in New Zealand. It began producing gas in 2006 and quickly became the largest gas producing field in New Zealand. However, Pohokura experienced large unplanned outages in 2018 which led to a national gas scarcity between September and November 2018 and high electricity spot prices for this period.

After those outages, gas production from the field declined quickly. In 2025, Pohokura was producing the least gas among New Zealand’s major gas fields. Figure 2 shows daily gas production at major fields from 2018 to now.

Gas scarcity is now one of the major challenges in New Zealand’s electricity sector, as experienced in August 2024. Continued decline in gas production has pushed up gas prices and increased the cost of gas-fuelled thermal generation. One of the tools used to counter gas scarcity has been for generators to temporarily buy gas from Methanex, which has long-term contracts for large volumes, but often this gas comes at a higher cost than the generators would otherwise pay.

Thermal generation costs heavily influence wholesale electricity spot prices

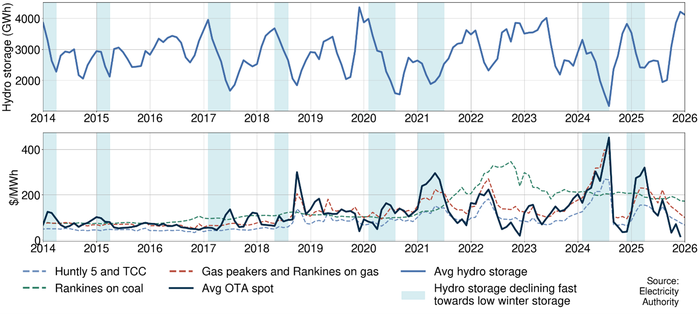

In general, average wholesale electricity spot prices closely follow the SRMCs of gas fuelled thermal generation (Figure 3). The correlation1 between the spot price and the cost of generating with any gas unit is strong, at 0.85. The correlation between the spot price and the cost of coal or diesel (not included in Figure 3) generation is weak - just under 0.3. There is a negative correlation of 0.51 between hydro storage and spot price, indicating that as hydro storage risks decrease, spot prices fall.

When hydro storage is declining quickly towards winter, this tends to push spot prices above gas and coal generation costs. This is because generators start pricing some energy from their hydro generation higher than thermal costs to encourage thermal generation to run in place of hydro generation and hence conserve water for the coming winter. These periods are shaded in blue in Figure 3. There is also some evidence that the sensitivity of spot electricity prices to periods of declining hydro storage has increased since 2018.

1The correlation coefficient ranges from 0 to 1 and describes the strength of a positive linear relationship, ie, the extent to which a movement in one value is reflected in a movement in the other. A value of 0 indicates no linear relationship, while 1 indicates a perfect one. It does not prove that change in one variable causes the change in another, but it is easily derived and helpful information.

Our new report provides insights into the hedge market

In the future, as more renewable generation is built, New Zealand's reliance on thermal fuels will decrease during times of high renewable generation. This has already occurred during summers when demand is lower, wind and inflows are higher and very little thermal generation is needed. That’s why towards the end of 2022, 2024 and 2025 wholesale prices dropped below the costs of thermal generation. However, thermal generation is still a key part of New Zealand’s electricity market, especially in winter.

The Government has indicated its plans to build an LNG import terminal to enable generators to access more gas for electricity generation when it is required. We will adjust our monitoring and reporting to include this new fuel as it comes into the system; it is not expected before 2027. We will then be able to extend our analysis to explain what impact it is having on electricity spot prices.

High-priced thermal fuel means periods of high spot prices. Participants can buy and sell hedges in advance to manage the risk caused by spot price volatility. The Electricity Authority publishes a monthly hedge market summary which reports on both ASX and over-the-counter hedge market activity. The purpose of this reporting is to make the hedge market easier to understand and support participants in making informed trading decisions.

Related News

Hedge market summary report – February 2026

We publish monthly hedge market summary reports to support transparency and build confidence in the market. The reports help electricity market participants un…

Deadline extended for non-discrimination obligations consultation

On 26 February, the Energy Competition Task Force launched a consultation on certain aspects of the proposed non-discrimination obligations, which are aimed at…

Next steps in our network pricing reform work

The Electricity Authority welcomes Transpower’s consultation for its operational review of the Transmission Pricing Methodology. Efficient network pricing is e…